I think Morgan Hill needs to drop something...any ideas?

http://bit.ly/s3y9CT

Ever wonder where our New Year's traditiions come from, why does the big ball drop, why do we drink champagne, why do we make resolutions now ? Interesting info here

When a homeowner goes thru a short sale or foreclosure there is some time that has to pass before they are eligible to get a home loan again. This has created demand for rentals and this has benefitted investors and builders....it's simply the principle of supply and demand.

I always ask my clients if they have littles or are planning on having them,that is important when considering a space and also general location as schools are a significant consideration.

Being a foodie from way back, I can spend a day looking thru recipe books, let me know what you think of this.

On this day in 1895, the world's first commercial movie screening takes place at the Grand Cafe in Paris. The film was made by Louis and Auguste Lumiere, two French brothers who developed a camera-projector called the Cinematographe. The Lumiere brothers unveiled their invention to the public in March 1895 with a brief film showing workers leaving the Lumiere factory. On December 28, the entrepreneurial siblings screened a series of short scenes from everyday French life and charged admission for the first time.

On December 27, 1932, in the height of the Great Depression, Radio City Music Hall opens! Proving a well known fact that stays true today, even during difficult times, music and dance will lift spirits and inspire and make people believe that things will get better.

Is today important in your history? Please share...

On Dec 26, 1946, Bugsy Siegel opened the Flamingo Hotel. The hotel was named after Siegel's girlfriend Virginia Hill, her nickname was "The Flamingo" because of her red hair and long legs....

Please share any item of interest that you know of from this day in history...

When home owners go thru a short sale or foreclosure there is a period of time before they can purchase property again. It is these good people who are now creating the demand in our rental market. It is likely we will see this demand for a minimum of 2 years.

Do you think distressed former home owners should be allowed to purchase a home less than 2 years after a short sale or 5 years after a foreclosure?

Are you thinking of purchasing a rental, check out the market by searching on Craigslist to see what other landlords are charging in rent for similar properties.

Principal reduction, is this too radical for lenders to wrap their heads around?

What do you think?

marks this wonderful African celebration centered around the principle of Unity in all things. I love the ideal of this holiday. Have a great day everyone.

My family has had a lot of money and health problems this year so Christmas is going to be a little tough. Still we are happy, healthy and together and that is what really matters!

This from a 12 year old child...

Ok, so my drink of choice is as follows:

Iced Grande 5 pump, non fat, no whip mocha

What's yours?

Love modern technology. Stay tuned to my You Tube channel for interesting insights and I love comments...

For crisper skin, unwrap the turkey the day before roasting and leave it uncovered in the refrigerator overnight. Need help tackling the big bird? Continue reading Food Network’s Top 10 Turkey Tips. Find the perfect turkey for your feast, starting with our most popular ever: Alton’s Good Eats Roast Turkey, an outstanding 5-star standby. Browse [...]

Investors Playing Major Role in Bay Area Housing Market

By Rick Turley

While the Bay Area housing market has had its ups and downs much of this year, a couple of segments of the market remained resilient through much of 2011. In previous columns, I’ve talked about the strong rebound in the luxury market from Silicon Valley up through Marin. But one other sector has also played an important role in keeping the overall real estate market going: the investment segment.

According to DataQuick, the La Jolla-based real estate information service, absentee buyers – real estate investors for the most part – bought one out of every five single-family homes and condos in August. Buyers paying cash accounted for more than a quarter of sales. And short sales – those transactions where a home sells for less than the homeowner owes on the mortgage – added up to another 20 percent of sales.

The trend has caught the attention of the local news media with the San Francisco Chronicle and San Jose Mercury both running long articles on the topic in recent weeks.

In her article, Chronicle reporter Carolyn Said noted that, “Real-estate investors have become a potent force in a moribund housing market…” She went on to say that, “despite record low interest rates, many consumers simply don't have enough confidence in their economic outlook to buy houses. Investors have kept prices from falling further…”

Today’s market is extremely attractive to investors. Record low mortgage interest rates, coupled with very favorable asking prices for distressed properties and other entry level homes, mean that rental income can easily cover the expenses for a new landlord owner. And given the volatility in the stock market and with other investments, real estate is looking like a better and better alternative.

While not everyone would agree, I think real estate investors are playing an important role in our market. When they buy, they’re often upgrading properties that in many cases are badly in need of maintenance. They’re helping to clear out the supply of vacant, bank-owned properties that can be a blight on neighborhoods. And in general, they’re reducing the huge inventory of distressed properties that serve to keep all home prices down.

"The market would be quite a bit sicker were it not for investors snapping up a lot of the properties," Andrew LePage, an analyst at DataQuick, told the Chronicle. "They account for a meaningful portion of the demand. To the extent to which there's at least a temporary floor under this market, they've helped to build it."

However, real estate investors – many of whom are paying all cash for entry-level properties – are making it hard for some first-time buyers and others to compete for those homes. Given the choice, it’s understandable that a seller would opt for a cash offer that’s likely to close quickly rather than take their chance that a buyer can secure mortgage financing.

Unlike past investors, today’s new landlords are generally not expecting to quickly flip a home for a profit, according to the Chronicle story. Instead, they see are seeking reasonable returns by simply owning and managing a rental property.

Realtors who work with these buyers say that many are first-time investors who like the long-term potential of investing in real estate over other investment vehicles. With prices and interest rates this low, they reason, there may never be a better time to jump in.

It’s also important to remember that most housing recoveries are preceded by a rise in rental housing rates. This has two effects, both positive for our housing recovery. The rise in rents attracts more investors as purchasers. As we noted earlier, they also unfortunately cause stiff competition among first-time buyers; but in some areas these investors are necessary to help stabilize hard-hit foreclosure areas and thus stabilize pricing. The other effect of rising rental rates? It causes more renters who qualify for homeownership to consider a purchase, especially with today’s interest rates.

As we approach a New Year, we are expecting more and more ofboth types of buyers in 2012 to come to the same conclusion.

Below is a market-by-market report from our local offices:

North Bay – Our Greenbrae office just reduced the price of a home in Kentfield in the $2.2 range and received multiple offers. Buyers are out there and perhaps coming out a little more aggressive in the search now. The Chronicle article on investors buying local homes has been encouraging for buyers to get into the market. In Northern Marin, agents are reporting a definite increase in open house traffic. We are seeing more multiple offers on well-priced properties. There has also been an increase in floor calls and walk-ins of interested buyers. In Petaluma, the competition is fierce for buyers in the under-$500,000 price range. The inventory is dwindling and well-priced properties are snatched up as they come on the market. With Sonoma County featured as one of the top 20 destinations by National Geographic, many buyers are trolling the open houses. First-time customers are becoming more and more common. The Santa Rosa market remains steady with some increase in REO inventory and a number of new escrows. Finally in Sebastopol, the majority of activity is in the lower end of the market with emphasis under $400k. One new listing in the country, priced at $399k, attracted over 22 groups. We are seeing a little activity in the move up range of $600-$800. Low appraisals continue to be problematic.

San Francisco– Our Lakeside office manager declares “outstanding lenders or cash” - that is what it takes to buy a home in this market. In spite of the dramatically low interest rates, deals are being held up by the lender’s increasingly high hurdles for property qualification. Buyers are being weighed down by poor lender choice. Still, we are finding a large number of cash buyers who can sail through transactions without the underwriting obstacles. Meanwhile, the Market Street office says sales activity is increasing and they finished a strong October with new transactions. The strategy seems to be price to sell or even price to induce multiple offers. The average list-to-contract time frame is less than three weeks, and on average they are selling at or slightly above asking price with 64% of the transactions seeing multiple offers. The Sunset office reports decreasing inventory but steady sales while the Van Ness office says inventory and sales activity have been steady in recent weeks.

SF Peninsula— Our Burlingame offices report that light inventory is fueling multiple offers for well-prepared and priced homes. There are waiting buyers out there. One home had over 200 attendees at open house and sold on the spot to a well-prepared buyer who had lost out in other recent multiple offers. The home had been carefully prepared and staged by the agent down to the last detail. In the Previews market, inventory is beginning to come off for the holidays if it has been on the market for a while, with sellers anticipating a better, more optimistic spring. At the same time there are some fabulous buys in Hillsborough at this time. Nov. Dec. could be the best time to negotiate with little competition. Across the hill in Half Moon Bay, the market has for $750k to $1m homes has been slow. However, homes in the $550k range move quickly, as do second homes over the $1.5m, sometimes for all cash. Our Menlo Park offices say inventory continues to be scarce. Open houses have been busy and the office is getting a lot of calls and walk-ins from interested buyers. In Palo Alto, the market changes on a weekly basis. In general, there’s very short inventory – including Palo Alto and surrounding communities, Mt. View particularly, compared to last year. The move-up market is slow and as a result we are slow to see new inventory. There also has been a serious lack of inventory, according to our Redwood City office, with most sales activity in the lower-price ranges. Sales activity has slow in the San Mateo market, possibly due to a lack of inventory, the uncertain economy or the upcoming holidays. Finally in Woodside, both inventory and sales activity are down in a fairly quiet market.

East Bay– Berkeley agents are busy working with buyers, getting price adjustments from sellers who want to move their properties, and telling renewed horror stories of appraisers creating obstacles by reading online disclosure packets and demanding repairs/clearances. Our Castro Valley office reports increasing inventory and steady sales activity. Inventory continues to decline in the Danville area while the buyers are becoming more active. Inventory stands at about 2 ¼ months in the San Ramon Valley - San Ramon and Danville are very active, while Alamo and Blackhawk are very slow. Our Livermore office reports inventory is increasing while sales are steady. In Fremont, both sales and listings are increasing. Our Oakland-Piedmont office says listings have picked up with clients making the decision to get their house sold before year-end. Open house activity was steady even at properties that have been held open for several weeks. Buyers are still being very discerning and don’t exhibit any urgency in writing an offer quickly. Our Orinda manager says it’s becoming more difficult to obtain loan docs and loan approval. Extensions of escrows are becoming more common. In Pleasanton, the local market has been steady with buyers still out there looking. Finally in Walnut Creek, our local office says inventory remains low and there are multiple offers on all well-priced properties.

Silicon Valley– Steady sales activity is reported in Cupertino. With inventory declining, open houses are busier than ever. In Los Altos, sales activity is increasing including a small increase in the $2 million and up market. Open houses are well attended at new single-family listings. Our Los Gatos manager says that overall, the high end continues to remain strong. Inventory remains low in most entry-level markets. The San Jose Almaden office says sales activity has been steady. Properties are selling, but buyers wish there was more to choose from. Pending sales in this region are 10% up over last year at this time but listings are down 33%. Low-end buyers are having trouble competing against all-cash or large-down payment buyers. All properly priced listings are getting multiple offers. The San Jose Main office also has seen a continued drop in inventory but activity at open houses is very strong. There are multiple offers on most homes in a variety of price ranges. Low interest rates and low inventory are main factors in the multiple offers we are currently experiencing. And our Willow Glen manager reports that regular sales are taking a little longer to close than expected and banks are slowly approving short sales. The Saratoga market seems like it’s slowing, which is normal this time of year.

South County– The Gilroy and Hollister markets both saw an uptick in REO listings coming onto the market. Open houses have been fairly well attended, but a lot of buyers are sitting on the fence. Sales are slow. Inventory is steady, but low for both markets. Gilroy has 3.3 months of inventory and Hollister has 3.6 months of inventory. Our Morgan Hill manager says that as the year winds down, the number of Morgan Hill listings has increased dramatically, but the ratio of listings to sales has decreased. In January 2011 there were only 138 listings available in Morgan Hill—with 27 closings (20%). October showed 311 listings with 51 closings (16%). While sales are up from the first months of 2011, a lower percentage of listings are actually selling. Prices on the other hand are down. The average sales price of a single-family home in Morgan Hill has dropped from a high of just under $600,000 to about $475,000 (a 25% differential). Morgan Hill remains a buyer’s market—many listings, good prices and great interest rates.

Santa Cruz – As we move into November and toward the end of the year and the holiday season, sales continue to be steady in the Santa Cruz area. There is definitely more activity in the under $600,000 price range, heavily influenced by short sales and REO business. We are finding some of the banks on the short sales are reacting much more quickly and we are seeing a shorter process with some of lenders, Chase being one of them. On “organic deals” financing is the biggest hurdle and agents need to pre-approve and counsel their clients through the buy process. Appraisals are all over the map, and we have had a couple of deals where the property did not appraise and the buyer and seller were able to come to a successful resolution and the sale went through. It is all about perceived value for the buyers. The home has to be a really good deal – and sometimes even then, the property may sit on the market.

Monterey Peninsula –The beat goes on with the steady activity in the Monterey Peninsula marketplace. These low mortgage rates seem to have brought some of those hanging-back buyers into the market, especially in the lower prices ranges. In looking through the lower priced homes in Seaside and Marina, for instance, we see that most of them are pending with very few “actives” on the market. And on the other end, the higher-priced properties, the volatility in the stock market may be contributing to increased sales there, many of them all cash. While we normally would be beginning to slow down about now, we continue to have a pretty consistent number of sales each week.

Shop for non-perishable goods now. You can buy flour, sugar, brown sugar, corn syrup, canned pumpkin, rice and cranberries, all before the crowds descend. Wait until the day before Thanksgiving to buy fresh vegetables, seafood and bread. Let the Thanksgiving Countdown Begin ? 2 Week Checklist Browse more of Food Network?s Thanksgiving recipes and tips.

This week brings us the release of six monthly economic reports for the markets to digest. With very important data scheduled for release two different days and relevant data four of the five days, we will likely see a fair amount of volatility in the markets and mortgage pricing this week.

There is nothing scheduled for release tomorrow, leaving the bond market to movement in stocks and overseas news. As of this evening, it appears that bonds are going to react negatively to news from Europe, meaning stocks may start the week off in positive ground. That can change between now and the opening bell tomorrow morning, but as of now it appears we may see some pressure in bonds and a possible increase to mortgage rates tomorrow.

The first data is one of the most important reports of the week. The Commerce Department will give us October's Retail Sales figures early Tuesday morning. This data measures consumer spending, which is considered extremely important to the markets because it makes up two-thirds of the U.S. economy. It is expected to show a 0.4% rise in spending, meaning consumers spent much less last month than they did in September. A larger increase would be considered negative news for bonds because large increases in spending fuels an economic recovery and raises inflation concerns in the marketplace. If Tuesday's report reveals a smaller than expected increase in spending, bonds should react favorably, pushing mortgage rates lower. If it shows a larger than expected increase, mortgage rates will likely move higher.

Also Tuesday is the release of October's Producer Price Index (PPI) from the Labor Department, which is one of the two key inflation readings on tap this week. The PPI measures inflationary pressures at the producer level of the economy. There are two portions of the index that are used- the overall reading and the core data reading. The core data is the more important of the two because it excludes more volatile food and energy prices. If it reveals stronger than expected readings, indicating that inflationary pressures are rising at the manufacturing level, the bond market will probably react negatively and cause mortgage rates to move higher. Analysts are expecting to see a 0.2% decline in the overall reading and a 0.1% increase in the core data.

Wednesday also has two reports scheduled that will likely influence mortgage rates. The first is October's Consumer Price Index (CPI) at 8:30 AM ET. This index is similar to Tuesday's PPI, except it measures inflationary pressures at the more important consumer level of the economy. We consider this report as one of the most important reports we get each month. The overall reading is expected to show no change from September’s level while the core data is expected to rise 0.1%. Weaker than expected readings would be good news for bonds and mortgage rates, while larger than forecasted increases could lead to higher mortgage rates Wednesday.

October’s Industrial Production data will be posted mid-morning Wednesday. It gives us a measurement of manufacturing sector strength by tracking output at U.S. factories, mines and utilities. It is expected to reveal a 0.4% increase in production, indicating moderate strength in the manufacturing sector. Stronger levels of production would be considered bad news for the bond market and mortgage rates, but this data is not as important as the CPI readings are. A significant surprise in the CPI would likely make this data a non-factor in Wednesday's mortgage pricing.

Thursday’s only monthly data is October's Housing Starts. This data gives us an indication of housing sector strength, but usually does not have a noticeable impact on mortgage rates. I don't expect this month's version to be any different unless it varies greatly from analysts' forecasts. It is expected to show a sizable decline in starts of new homes.

The final report of the week will come from the Conference Board late Friday morning when they release their Leading Economic Indicators (LEI) for October. This is a moderately important report that attempts to predict economic activity over the next three to six months. It is expected to show a 0.6% increase, meaning economic activity will rise fairly rapidly over the next couple of months. Generally speaking, this would be bad news for bonds. However, since this data is considered only moderately important, its results need to vary by a wide margin from forecasts for it to affect mortgage rates.

Overall, look for Tuesday or Wednesday to be the most important with very important reports scheduled those days. It is difficult to label any particular day as the quietest day, but Thursday is a good candidate. The key releases will be Tuesday's Retail Sales and Wednesday's CPI reports. They will probably determine whether rates close the week higher or lower than tomorrow's opening levels. Since this is likely to be a fairly active week for mortgage rates, it would be prudent to maintain regular contact with your mortgage professional if still floating an interest rate.

Information courtesy of Joe Patterson with Princeton Capital. (408)674-7438.

As the "bike messenger" announced the various properties, in every neighborhood from Saratoga to South San Jose, no one bid on the properties. So when no bids were received the bank just took the property back and the foreclosure sale was complete on those properties. That happened with 99% of the list. However, when the home my client was interested in was announced, there were three different bidders. The auction bids started at 245K and the winning bid was 245,100. The bidder did not have to go higher and that lucky investor won the property. As my client went largely to see how the process worked he did not move forward on the bid. I would still be cautious before investing in an auction home unless you have done a previous title search. It can be costly to clear secondary liens and tax liens and those must be cleared or satisfied for title to be clear and to transfer title to a subsequent buyer in a flip.

If you are an investor with a team of rehab specialists and with some title support, then an auction may be a good option. My advice, gather as much information on the property prior to auction and then move forward with eyes wide open.

Thoughts...?

"I always like to see a front door with a fresh coat of paint. It makes a home really welcoming. Just sand down any old lumps or peeling paint patches, then brush on some exterior paint (semigloss) in a color that stands out."

There are so many beautiful (and strange-looking) squash at the market right now. Sure, they’re great for a table centerpiece for Thanksgiving, but why not cook with them as well? Turn acorn, butternut, fairytale (yes, fairytale) and more into a delicious fall soup. Add in some pumpkin and you’re cooking the best of what fall [...]

I accompanied an investor client recently to the courtroom steps in downtown San Jose. He had his eye on a Victorian that was going to auction. The home was recently sale pending at a price of $300,000 but the bank was auctioning the home for $245,000. The experience itself is one worth noting. As there are many steps in the process to buying a home at auction, I will be sharing the process in several blogs and would love to hear of anyone else's auction experiences. As a Realtor, this is not our stage, but many of my clients are now purchasing at Auction and then holding the properties as investments or selling them for a profit (aka flipping).

When we arrived we were the only ones at the back of the courthouse downtown and there was no indication that this was the place. After awhile, a gentleman who looked like a bike messenger joined us. He did not indicate that he was the auctioneer, a competing buyer or otherwise. He just showed up. As 10am approached, the auction hour published by the trustee...several more people arrived, it was a very eclectic group. At 10am, the "bike messenger" opened a black notebook and announced that he would read the properties for sale at auction that day, and he told us quickly that a prospective buyer would need to present good funds, a cashiers check, for the exact bid amount. As a Realtor, this was all a bit suspicious, this did not appear to be a person licensed to sell or auction Real Estate, no business cards, no name tags, no company reputations to give us any sense of security. Yet, my client was expected to present his cashiers check to this gentlemen and then be prepared to take ownership immediately. There are no disclosures, no title reports, no tax statements, Nada! I suppose that goes against my grain as the details are the key to protecting my clients. Stay tuned for more of the auction experience. Again, I welcome your comments.

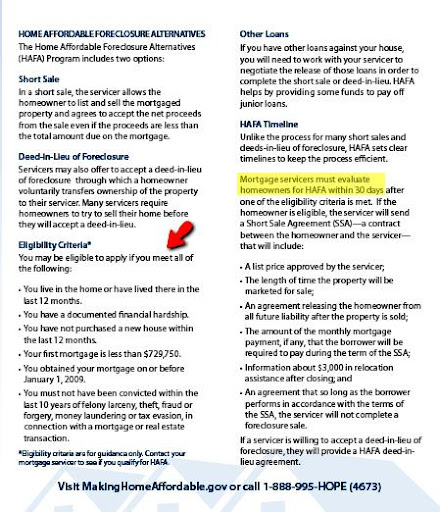

As a homeowner you should carefully consider your options as soon as you experience challenges when it comes to your financial ability to maintain your home (see “Know Your Options” on this website). Many of the options are geared … Continue reading

Gavilan College in Gilroy has been awarded $6 million from the U.S. Department of Education for a program to aid Hispanic and low-income students generally in science and technology instructional areas, among other topics. The campus will receive $1.2 million annually over the next five years for a program titled ?STEM Magnet: Improving Pathways for Hispanic/Low-Income Students.? STEM is an acronym for the Science, Technology, Engineering and Mathematics Education Coalition, an organization that seeks to strengthen academic programs in those subject areas to upgrade workforce development in higher education...

It can certainly be overwhelming to keep up with every bit of news affecting the real estate industry. When it comes to distressed properties I try very hard to push out the information as soon as news breaks! Today I am … Continue reading

Here are the latest market statistics, let me know if you want to know the value of your home. No obligation, knowledge is a powerful tool!

Be honest. You have pumpkins on your porch and candy corn in your hand right this very minute, but you’re already secretly thinking about your Christmas decorations. It’s okay. You’re not alone. For those who enjoy holiday cheer a little early, here are some simple handmade Christmas ornaments and decor to keep you satisfied until [...] Related posts:

Tesla Motors Inc. is opening the doors of its huge, gleaming new Fremont factory this weekend to give buyers of the company's Model S Sedan their first good look at the highly-anticipated electric car. At two separate events on Saturday and Sunday evenings, buyers get to take short rides in the Model S, tour the factory to see how it is made and learn some details about the car's features from Tesla CEO Elon Musk. The electric car maker (NASDAQ:TSLA) is headquartered in Palo Alto. The car's buyers have put down $5,000 deposits - or $40,000 for the "signature series," the first 1,000 cars off the line - but won't actually receive their cars until next summer at the earliest...

Tesla Motors Inc. is opening the doors of its huge, gleaming new Fremont factory this weekend to give buyers of the company's Model S Sedan their first good look at the highly-anticipated electric car. At two separate events on Saturday and Sunday evenings, buyers get to take short rides in the Model S, tour the factory to see how it is made and learn some details about the car's features from Tesla CEO Elon Musk. The electric car maker (NASDAQ:TSLA) is headquartered in Palo Alto. The car's buyers have put down $5,000 deposits - or $40,000 for the "signature series," the first 1,000 cars off the line - but won't actually receive their cars until next summer at the earliest...

This week brings us the release of only three monthly economic reports that are likely to influence mortgage rates. However, two of those three releases are extremely important to the financial and mortgage markets and we also have a congressional appearance by Fed Chairman Bernanke. We start the week with one of the highly important reports and end it with the other. In between, we will watch Chairman Bernanke’s testimony and stock movement for mortgage rates direction.

Tomorrow has the Institute for Supply Management (ISM) posting their manufacturing index for September at 10:00 AM ET. This index measures manufacturer sentiment and it can be heavily influential on the markets and mortgage rates. Analysts are expecting to see little change from August’s 50.6 reading, meaning surveyed manufacturers felt business conditions were steady from the previous month. The 50.0 benchmark is extremely important because a reading above that level means more surveyed executives felt business improved than those who said it had worsened. This data is important not only because it measures manufacturer sentiment, but it is also very recent data. Some economic releases track data that are 30-60 days old, but the ISM index is only a few weeks old. If it reveals a reading below 50.5, meaning sentiment fell short of expectations, we should see the bond market move higher and mortgage rates fall tomorrow.

Tuesday’s data will come from the Commerce Department, who will post August's Factory Orders data at 10:00 AM ET. This manufacturing sector report is similar to last week's Durable Goods Orders release, but also includes orders for non-durable goods. It can impact the bond market enough to change mortgage rates if it varies from forecasts by a wide margin. Analysts are forecasting a decline of 0.1% in new orders, meaning manufacturing activity slowed in August. This would be good news for the bond market and mortgage pricing, but I believe we will need to see a much larger decline than 0.1% for this data to create an improvement in rates.

Chairman Bernanke’s testimony will take place late Tuesday morning. He will speak before a joint congressional committee about the economy and monetary policy. As is the case whenever he speaks publicly, all eyes will be on his words. I am sure he will be drilled from members of the committee about the Fed’s intentions on getting the economy moving. It will be interesting to see what type of questions get thrown at him. Market participants will be looking for any indication of what their next move will be. There is a high likelihood of seeing a good deal of volatility during his testimony and the Q&A portion that will follow.

Wednesday and Thursday have nothing of concern scheduled. There are a couple of private sector reports due to be posted, but none of them have the potential to cause significant movement in mortgage rates. We will get last week's unemployment numbers from the Labor Department Thursday morning, but since it tracks only a single week's worth of new claims, its impact on the markets and mortgage rates is usually minimal. Worth noting though is the fact that this Thursday's report will cover the last week of the month that Friday's monthly report will include. Therefore, a significant surprise in Thursday's numbers could cause some analysts to revise their estimates for Friday's report and may influence mortgage rates slightly.

The Labor Department will post September's Employment report early Friday morning. This report will reveal the U.S. unemployment rate, number of new payrolls added or lost during the month and average hourly earnings. These are considered to be very important readings of the employment sector and can have a huge impact on the financial markets. The ideal scenario for the bond market is rising unemployment, falling payrolls and a drop in earnings.

If this report gives us weaker than expected readings, bond prices should move higher and we should see lower mortgage rates Friday. However, stronger than forecasted readings could cause a sizable spike in mortgage pricing. Analysts are expecting to see the unemployment rate remain at 9.1%, an increase of 63,000 new jobs from August's level and a 0.2% increase in earnings.

Overall, I suspect we will see a fair amount of volatility in the markets and mortgage rates this week. There isn’t that much data being released, but what is being posted is extremely important to the markets and highly influential on mortgage pricing. Labeling Tuesday and Friday as the most important days is easy due to Mr. Bernanke’s speech and the importance of the Employment report. Tomorrow will also probably be an active day for mortgage rates, so maintain fairly constant contact with your mortgage professional this week if still floating an interest rate.

Thanks Joe Patterson for your wonderful insights. Joe Patterson is with Princeton Capital and can be reached at (408)674-7438

Ladies, don your dirndls, and gentlemen, fasten your lederhosen, because Oktoberfest 2011 is officially underway. Though this beer barrel-tapping festival runs from September 17 through October 3 in Munich, Germany, you can bring the party stateside with our comprehensive guide to everything Oktoberfest, which includes clever (and useful) German phrases, a traditional Oktoberfest menu, classic [...]

Yesterday, kids and parents tuned into Sesame Street?s 42nd season on PBS. Yesterday, I also found these adorable Bert and Ernie pumpkins on the Craft blog. Coincidence? I don’t think so. (It’s no coincidence that everyone loves Sesame Street, right?) I think it’s clever that the jack-o’-lanterns go beyond simple carving, and employ paint, faux fur, [...] Related posts:

What is Deed-for-Lease? The Deed-For-Lease? option is a program from Fannie Mae that allows you to lease your home after you have transferred the title to your property to the mortgage company (commonly called a Deed-in-Lieu of Foreclosure). The lease … Continue reading

In my early twenties, I moved from my hometown of Portland, Ore. to Philadelphia. It was a big move, made even more challenging by the fact that I only knew one person my own age in the entire city (as lovely as it was to be near my 86-year-old grandmother, eating dinner with her at [...]

From the use of bold and bright pattern to walls painted in zesty colors, these joyful designs make for a happier home.

How do you get your child into a school both of you love? In the case of private schools, the admissions process is clearly stated in the applications. In districts with only neighborhood schools, enrolling can be as straightforward as heading down to the local district office or school and signing up.

Q. I am considering purchasing a home; my Realtor® tells me much of the current inventory is Short Sales or REOs and Foreclosures; what is the difference? A. Foreclosure is a legal process by which a defaulting borrower is deprived of their interest in the property. It is not a type of property. Real Estate [...]

Reports are rolling in that seem to confirm that Apple's next-generation iPhone will land next month, setting the blogs and rumor mills abuzz. Exactly when the iPhone 5 will be in stores is not known, with some saying the first week of October and others saying not until the second half of the month. There are also conflicting reports on whether there will be one or two new iPhones, a state of the art iPhone 5 and an entry level iPhone 4G S that will sell for less. The latest on this comes in a report that European iPhone service provider Vodafone has four iPhone 5 models listed for sale next month, with 16GB and 32GB and in black or white, but with no mention of an iPhone 4G S.

BEIJING (Reuters) - Ford Motor plans to more than double its offers across vehicle segments in China, the world's top market, as it speeds up the launch of new models, a senior executive said on Saturday.

Bank of America and JPMorgan Chase & Co. haven’t done enough to help people permanently lower their mortgage payments and avoid foreclosure, the Treasury Department said Thursday.

If you're planning to sell your house any time soon, home improvements that build property value should be on your to-do list.

Fewer people applied for unemployment benefits last week, following the end of a strike by Verizon workers. Applications fell 12,000 to a seasonally adjusted 409,000 last week, the first decline in three weeks, the Labor Department said Thursday.

This week brings us the release of four relevant economic reports in addition to another FOMC meeting and two relevant Treasury auctions. With all of the volatility in the markets of the past two weeks, it is difficult to say whether this will be an active week for mortgage rates. Under normal circumstances, it would be. But it is hard to label any week as active if comparing to the previous two.

There is nothing of importance scheduled for release tomorrow, but we do have Friday evening’s Standard & Poor’s downgrade of our credit rating to deal with. The action was announced after the market’s closed, so we have not had an opportunity to see our markets react to the news. Overseas stock markets have reacted negatively to the news, so there is little to be optimistic about towards our opening bell tomorrow. It is fairly safe to assume that stocks will open lower, but what will the bond market do? Logic would tell us that the downgrade is certainly negative news for bonds as it is those debts that there is question about our ability to repay. However, the same theory should have prevailed over the past two weeks but did not as investors sought safety in bonds from the stock selling. So, what will we see tomorrow morning? This is just a guess, but I am thinking we will see stocks and bonds in negative ground, meaning higher mortgage rates.

The first economic data of the week is Employee Productivity and Costs data for the second quarter that will be released Tuesday morning. It will give us an indication of employee output per hour. High levels of productivity are believed to allow the economy to grow without fears of inflation. I don't see this being a big mover of mortgage pricing, but since it is the only data of the day it may influence rates slightly during morning trading. Analysts are currently expecting to see a decline in productivity of 0.6% and a 2.2% jump in labor costs. A stronger than expected productivity reading and a smaller than expected increase in costs could help improve bonds, leading to lower mortgage rates Tuesday.

The FOMC meeting is a single-day event that will be held Tuesday and will adjourn at 2:15 PM ET. It is expected to yield no change to key interest rates. Usually, the post-meeting comments seem to have more of an influence on the markets than the rate adjustments themselves, or a lack of one in many cases. Look for the statement to lead to volatility during afternoon trading if it hints at what the Fed's next move may be and when it will come. Market participants will be looking for any indication of a move to help boost economic activity. If the statement does not give us new information, mortgage rates will probably move little after its release.

There is no important economic data on the calendar for Wednesday. June's Trade Balance report will be released early Thursday morning. It gives us the size of the U.S. trade deficit but is the week's least important report and likely will have little impact on the bond market and mortgage rates. Analysts are expecting to see a $48.0 billion deficit, but it will take a wide variance to directly influence mortgage pricing.

Friday has the remaining two pieces of economic data, one of which is highly important to the markets and mortgage rates. July's Retail Sales data is that report. This data is very important to the financial markets and mortgage rates because it helps us measure consumer spending. Since consumer spending makes up two-thirds of the U.S. economy, any data related to it can cause a fair amount of movement in the markets. A smaller than expected increase would indicate that consumers are spending less than previously thought, potentially further slowing the economic recovery. This is good news for the bond market and mortgage rates as it eases inflation concerns and makes long-term securities such as mortgage-related bonds more attractive to investors. Current forecasts are calling for an increase of 0.5%.

The last report of the day will come from the University of Michigan, who will release their Index of Consumer Sentiment for August at 9:55 AM. This index gives us a measurement of consumer willingness to spend. If confidence is rising, then consumers are more apt to make large purchases. This helps fuel consumer spending and economic growth. By theory, a drop in confidence should boost bond prices, but this data is considered moderately important and carries much less significance than the Retail Sales report does. Analysts are expecting to see a reading of 62.5, which would be a decline from July’s revised reading.

Also worth noting are two important Treasury auctions this week. The sale of 10-year Notes will be held Wednesday while 30-year Bonds will be sold Thursday. We often see some weakness in bonds ahead of the sales as the firms participating prepare for them. However, as long as they are met with decent demand from investors, the firms usually buy them back. This tends to help recover any presale losses. But, if the sales are met with a lackluster interest from investors- particularly international buyers, the bond market may move lower after the results are posted and mortgage rates may move higher. Those results will be announced at 1:00 PM each sale day.

Overall, it is difficult to label one particular day as the most important. Friday’s sales data is the most important economic report, but Tuesday’s FOMC meeting has the potential to cause plenty of movement in the markets and mortgage pricing also. Tomorrow will also be interesting, especially considering the size of the sell-off in bonds Friday. I would not be surprised to see that negative tone extend into tomorrow’s bond trading and mortgage rates. I suspect the FOMC meeting will not have as much of an influence on mortgage rates as one may expect, but the markets can react wildly to a single word or omission of a word in the statement, so we need to be cautious. This is certainly another week that continuous contact with your mortgage professional is highly recommended if you are still floating an interest rate.

Without congressional action by Tuesday to raise the debt limit, the Treasury would no longer be able to borrow and thus would not be able to pay all its bills.

The National Association of Realtors will post June's Existing Home Sales figures late Wednesday morning. This report gives us a measurement of housing sector strength and mortgage credit demand, but as with all of this week's data it is not considered highly important. Current forecasts are calling for a small increase in sales from May's totals. A drop in sales would be considered good news for bonds and mortgage rates because a weak housing sector would make it difficult for the economy to recover anytime soon. However, unless this data varies greatly from forecasts it probably will lead to only a minor change in mortgage rates.

June's Leading Economic Indicators (LEI) will be posted at 10:00 AM Thursday. This Conference Board index attempts to measure economic activity over the next three to six months. While it is not a factual report, it still is considered to be of moderate importance to the bond market. It is expected to show a 0.3% increase, meaning that we may see a gain in economic activity over the next few months. A smaller rise in the index would be good news for the bond and mortgage markets.

Overall, this is a moderately significant week for the bond market and mortgage rates. With no highly important economic data to drive the markets and mortgage pricing, we likely will see the stock markets influence mortgage rates. If the major stock indexes rally, funds will probably move away from bonds, driving yields and mortgage rates higher. But weakness in stocks would fuel bond buying and lower mortgage rates for borrowers. I am going to remain pessimistic towards rates, at least near term until the 10-year Note yield remains under 3.00% for some time. It is my opinion that we are more likely to see it move back above 3.00% before we see a new downward trend start. Accordingly, this leads me to remain cautious towards rates, at least for the time being.

If I were considering financing/refinancing a home, I would.... Lock if my closing was taking place within 7 days... Lock if my closing was taking place between 8 and 20 days... Lock if my closing was taking place between 21 and 60 days... Float if my closing was taking place over 60 days from now...

Create a home inventory before disaster strikes to make filing an insurance claim a smoother process.

Avoid fence disputes by practicing fence etiquette—a good neighbor policy. If you follow zoning regulations and share basics with neighbors before construction, you can install a new fence AND stay on good terms with the folks next door.

Facebook investor and Russian billionaire Yuri Milner made worldwide headlines recently when he purchased a Los Altos Hills estate for a reported $100 million, the most expensive residential real estate deal in the U.S. But while Milner’s purchase caught the attention of reporters here at home and the paparazzi around the world, he’s not the only foreign buyer to be placing bets on the Bay Area housing market.

Silicon Valley, Hillsborough, San Francisco and other parts of the Bay are attracting growing interest from offshore investors these days. We’re seeing it in our own offices on the Peninsula and in Silicon Valley. The foreign buyers are usually looking for upscale, single-family homes and often pay for multi-million-dollar purchases in cash. Unlike Milner, most of the foreign buyers aren’t seeing their deals reported in the news media – and that’s just fine with them as they truly value their privacy.

The offshore buyers are buying here for a number of reasons, according to recent studies and our own agents who have represent them: U.S. homes are generally less expensive than comparable foreign properties. Investors understand that U.S. real estate prices are unusually low right now, and in the long run could be a great investment. Additionally, the U.S. is looked upon as a more secure and stabile place to own property. Finally, some buyers are concerned with the financial markets and believe that investing in real estate over the long run will be a much wiser investment.

Our Burlingame North Office had a number of recent sales to Chinese buyers – all for several million dollars and all in cash. The investors used profits from antiques, commodities and other investments to funnel into the real estate market. One Peninsula listing received seven offers – four of which were all-cash offers from China buyers. A Chinese investor, with family and interpreter in tow, bought two houses in Pebble Beach, one on 17 Mile Drive, another above The Lodge, for $7 million and $10 million in March.

What’s driving the Chinese interest in U.S. real estate? One of the fundamental reasons, we’re told, is that you can’t buy fee-simple real estate in China like you can in the U.S. As a result, no matter whether you’re purchasing a single-family home or a condo, you cannot own the land underneath your home. The land is always leasehold property held by the Chinese government.

Silicon Valley and the Bay Area are considered highly attractive to foreign investors. Obviously, having the world’s leading technology hub in our backyard doesn’t hurt. Our tech industry is attracting top-flight engineers and other highly educated, well-paid professionals from around the world. The growing field of tech startups and tech IPOs are attracting some of the world’s wealthiest investors. Having two world-class universities in Stanford and Cal has also proven to be a strong magnate, as we’ve noted in past columns. San Francisco and the Bay Area have always been popular destinations for people around the globe. And finally, real estate in the Bay Area has a long track record of being a good investment for patient buyers. These offshore buyers fully appreciate that.

A recent study by the National Association of Realtors found that international purchases in the U.S. surged by $16 billion last year, the highest gains in recent years. “The U.S. has always been a desirable place to own property and a profitable investment,” said NAR President Ron Phipps, “In recent years we have seen more and more foreign buyers coming here to take advantage of low prices and plentiful inventory.”

Recent international buyers came from 70 different countries, up from 53 countries the previous year. Canadians accounted for the largest percentage of international purchases with 23 percent, while Chinese buyers were second with nine percent. Tied for third were Mexico, the U.K., and India. Argentina and Brazil combined reported an increase in foreign sales with five percent, up from two percent in 2010.

Not surprisingly, California was among the top states in attracting foreign buyers. But Florida actually was number one with 31 percent of total foreign transactions. California was second with 12 percent, Texas was third with nine percent, and Arizona fourth with six percent. Generally, the East Coast attracts European buyers. The West Coast remains popular for Asian purchasers. Mexican buyers are traditionally attracted to the Southwestern markets. And Florida is most popular among South Americans, Europeans and Canadians.

If you’re interested in learning more about the trend in international homebuyers, the NAR report is available here.

Below is a market-by-market report from our local offices:

North Bay – In Southern Marin, there has been a slight slowdown, both in open house attendance and sales. Many are attributing it to Father’s Day and graduations, and trying to be optimistic that we are not already in a seasonal summer slowdown. But on the plus side, there has been an increase in the number of high-end sales ($3 million and above) in the south part of the county. Our Greenbrae office says that inventory has declined but sales activity is steady. In Northern Mark, the lower end of the market continues to be the strongest, with either investors paying all cash or owner-occupiers utilizing FHA loans. We continue to see first-time buyers who are now looking further afield (Petaluma, Vallejo, etc.) for homes. Our Petaluma office reports that sales have been steady with double digit multiple offers in the under $300,000 range. Activity is also starting to heat up in the $400,000 to $800,000 range. Both sales and inventory are on the rise in Santa Rosa. Although buyers and sellers seem to be spending a lot of time sitting on the fence, the local market is slowly getting more active. In Sebastopol, open houses are well attended and the market remains steady overall. Most agents are involved in multiple offers. Cash is king when it comes to winning out.

San Francisco – Our Lombard office reports that sales activity has been steady with most deals resulting from multiple-offer situations and prices over asking. On the flip side, open houses and broker traffic have been slower, possibly a sign of the early summer slowdown. Our Market Street manager says the saying the “first offer is the best offer” is turning out to be quite true. Coaching sellers to act fast and respond to interest when the property is first listed is paramount. It’s often the first party with an offer that has the best terms and price. Sellers who wait often find themselves losing the first interested party in hopes of getting additional interest. Our Sunset office says open houses are still well attended but buyers are a little bit more reserved when it is time to make an offer. The summer slowdown is starting to show. Pricing is still the key in all markets.

SF Peninsula — Our Burlingame office said the local market has slowed recently, which generally corresponds with the end of school and summer vacations. Across the hills in Half Moon Bay, there has been good activity on the coast. The hottest segment is from $550k-$650k three-bed, two-bath and not a distressed property. Our Menlo Park office says the local market is still very strong with healthy sales volume. Lending is getting more onerous (conditions, etc.) but loans are out there. In Portola Valley, there have been a couple of bigger sales recently and still lots of strong buyers, but they’re being very cautious, our local manager reports. In Redwood City and San Carlos, activity seems to be picking up. Offers are taking longer to put together but with persistence they are coming together and closing. Selling still seems to be about location, condition and mostly price. If priced right, particularly in San Carlos, the properties go into contract quickly. In San Mateo, it’s a mixed market with single-family residences doing well but the condo market is still soft. It’s even more challenging because of banks looking at delinquent homeowners association dues and the ratio of owner-occupied units to renters.

East Bay – In Castro Valley, the market has quieted with inventory declining but sales steady. The market in Livermore for detached homes remains strong with less than three months inventory. Some 69% of the detached homes that are pending since June 1 were listed below $600,000. Most of the pending sales in Livermore in the $200,000 to $400,000 price range are multiple offers. Open house activity was lighter over the weekend, according to our Oakland/Piedmont office. But potential buyers were indicated that they were ready to buy if they found the right house. There is not a sense of urgency with the buyers so they are looking until they find the “perfect” house while investors are still looking for the best prices. In the Lamorinda area, the market has been steady of late. New listings and sales remain strong. However, It is very area specific. Some listings sell the moment they hit the market while others seem to take much more time. Finally in Walnut Creek, it’s steady as she goes. Open house activity has been good. Buyers seem to be out there looking, but many are hesitant to move ahead with purchases.

Silicon Valley – The Cupertino market has been much slower than usual with lots of agents on vacation. The Previews high-end market has been flat as well. Both sales and inventory are on the rise in Los Altos. Buyers are attending open houses in good numbers. Some are cautious while others are jumping in, especially in the single-family home market in Los Altos and Palo Alto. The Los Gatos market has been steady with inventory increasing, according to our local manager. Palo Alto remains a red-hot market with sales continuing to rise and inventory drop. Multiple offers in excess of 30% over list price are not uncommon in some areas due to the short supply and strong demand. Our San Jose Almaden manager says open house activity is starting to resume again. There were 54 groups through one house over the weekend in Willow Glen and 28 through one in Almaden. The Willow Glen office says sales are starting to pick up as compared to one to two weeks ago. The Saratoga market has been steady, tracking closely to what our local office sees this time of year. Our manager reports that they’re still seeing multiple offers for the under $2 million market in Saratoga and the Cupertino market.

South County – The last two weeks has seen a decrease in ratified contracts and buyer traffic, according to our Gilroy office. Traditionally, this happens at this time of year due to the end of school, graduations and vacations. However, with recent negative media coverage it seems the slowdown is a bit deeper. Best quote of the week: “Real Estate is local and consumer confidence is national.” Our Morgan Hill manager said that the local market continues to take one step forward and two steps back. March, April and May were very good sales month, but by the first of June sales activity slowed dramatically. This slowdown sometimes is attributed to the “June Swoon”—graduations, vacations, and end of school. In this case, however, he said national economic news, gas prices and the job market are also contributing factors. The market continues to be attractive to cash investors who are buying and either renting or “flipping” discounted properties.

Santa Cruz – Closed sales overall in the county were down 18 percent in May from a year ago while the median sale price has declined to just under $450,000. The good news is that there are significantly more properties under contract than there were a year ago, up 47%, and less inventory available, down by 8%. Nearly 60% of the properties closing are $500,000 or less with a high percentage of short sales and REO’s. Pricing and the buyer’s perception that the home is a great value is the driving force. It’s critical for sellers to price appropriately at the beginning. In the Previews segment of the market, sales over $1 million in Santa Cruz County totaled 10 in May vs. seven a year ago. The overall percentage of homes over $1 million is up from 4% to 7% of the total sales, a good sign. In the over $2 million mark, there are currently 52 homes on the market and two that sold in May. The market time for these homes is half of what it was a year ago, which is a sign that the high-end buyers are recognizing the time is right for that once in a lifetime purchase of a second home.

Monterey Peninsula – Our local offices report that they’ve had a busy May, putting 82 properties into escrow including several all cash sales with quick closes of only 7-10 days. By comparison, the first half of June feels a little less active. However, the area is filled with visitors now. Open houses are good with lots of showings of properties going on, so we’re expecting to see more new sales in coming weeks. The local inventory has gone down considerably since the beginning of the year, when we reached the highest point in January for the past two years. We are now at a new low of only about 21 months’ supply of inventory in our primary coastal market (not including Seaside or Marina). Those communities are down to a four-month supply. With the selection of properties not as good, quick action and even multiple offers happen on desirable, priced-right properties coming onto market.

That’s it for now. Have a good week!

Rick

Rick Turley is the President of Coldwell Banker Western Region

Real estate experts and agents say the uptick in mega-estate sales may portend a turnaround in the broader housing market.

This week brings us the release of seven important economic reports for the bond market to digest in addition to the minutes from the last FOMC meeting, two relevant Treasury auctions and semi-annual Congressional testimony by Fed Chairman Bernanke. Several of the economic reports are considered to be of high importance, meaning we will likely see more volatility in the financial markets and mortgage pricing over the next several days. There are also some heavily watched corporate earnings releases scheduled for the stock markets this week that can influence bond trading and therefore, mortgage pricing. In other words, we are in for a heck of a week.

The first data of the week is May's Goods and Services Trade Balance report early Tuesday morning, which measures the size of the U.S. trade deficit. This data is not considered to be of high importance to the bond market and will not likely have an impact on mortgage rates. However, if it does vary greatly from analysts' forecasts of a $44.0 billion deficit, we may see some movement in bond prices and possibly a slight change in mortgage pricing. This is the least important of this week’s economic data.

Also worth noting about Tuesday is the afternoon release of the minutes from the last FOMC meeting. There is a possibility of the markets reacting to them following their 2:00 PM ET release, especially if they show unexpected dissention among some of its members during discussion and voting at the last meeting or give any indication of the Fed's possible next move with monetary policy.

There is no relevant economic data scheduled for release Wednesday, but Fed Chairman Bernanke will present his semi-annual update about the economy and monetary policy before Congress. He will speak before the House Financial Services Committee Wednesday and the Senate Banking Committee Thursday, each at 10:00am ET. His testimony will be broadcast and watched very closely. Analysts and traders will be looking for the status of the economy and his expectations of future growth, particularly inflation and unemployment concerns that will lead to changes in key short-term interest rates. This should create a great deal of volatility in the markets during the prepared testimony and the question and answer session that follows. If he indicates that inflation may become a point of concern or anything that hints at rapid economic growth, we can expect to see the bond market fall and mortgage rates rise Wednesday.

We usually see the most movement in rates during the first day of this testimony as the Chairman's prepared words for both appearances are quite similar to each other, meaning that the second day of testimony rarely gives us anything we did not hear during the first day. The general exception is something asked or answered during the Q&A portion of the second day's appearance.

Wednesday also starts the first of the two important Treasury auctions when 10-year Notes will be sold. That sale will be followed by a 30-year Bond auction Thursday. These sales can influence market trading in bonds and possibly affect mortgage rates. If the sales are met with a strong demand from investors, particularly Wednesday's sale, we should see afternoon improvements in bonds that could lead to downward revisions to mortgage rates. However, if concern about the amount of debt that is being sold keeps buyers on the sidelines, we may see bonds fall after results are posted at 1:00 PM ET and mortgage rates move higher those days.

In addition to the second day of testimony and the 30-year Bond auction, Thursday does have some key economic data being posted. The first is June's Producer Price Index (PPI) from the Labor Department. It is a very important release because it measures inflationary pressures at the producer level of the economy. It is expected to show a 0.3% decline in the overall reading and a 0.2% increase in the core data reading. The core reading is the more important of the two because it excludes more volatile food and energy prices. The bond market should react quite favorably if we get weaker than expected readings, but a larger than expected rise in the core reading could send mortgage rates higher Thursday.

June's Retail Sales report will also be posted at 8:30 AM ET Thursday morning. This data is considered to be of high importance because it measures consumer spending. Consumer spending makes up two-thirds of the U.S. economy, so any related data is watched closely. The Commerce Department is expected to say that sales at retail establishments fell 0.2% last month. A larger than expected decline in sales could help fuel a bond rally and lead to lower mortgage rates because it would mean that the economy is likely weaker than thought.

Friday has the remaining three economic releases, beginning with what arguably is the single most important monthly report for the bond market. That is June's Consumer Price Index (CPI) at 8:30 AM ET, which is a mirror of Thursday's PPI with the exception that the CPI measures inflation at the more important consumer level of the economy. Analysts have forecasted a 0.1% decline in the overall index and a 0.2% rise in the core data. The core data is considered to be the key reading because it gives us a more stable measure of inflation. Higher than expected readings could raise inflation fears and push mortgage rates higher, while readings that fall short of forecasts should lead to lower rates Friday.

June's Industrial Production data is the second report of the day at 9:15 AM ET. This data measures output at U.S. factories, mines and utilities, giving us an indication of manufacturing sector strength. It is expected to show a 0.2% rise in production, indicating that the manufacturing sector strengthened slightly during the month. That would basically be bad news for bonds, however, the CPI will take center stage Friday morning.

The final report of the week is the University of Michigan's Index of Consumer Sentiment. This index is released in a preliminary form each month and then followed up two weeks later with a final reading. The preliminary reading for July will be posted late Friday morning and is expected to drop slightly from June's final reading of 71.5. This would indicate that consumers were a little less comfortable with their own financial situations this month than last month. It is believed that if consumers are confident in their own finances, they are more apt to make large purchases in the near future. And with consumer spending making up two-thirds of our economy, investors pay close attention to reports such as these. So, a decline in confidence would be good news for mortgage rates because it means many consumers will probably delay making a large purchase in the immediate future, limiting economic activity.

Also worth noting is the fact that tomorrow kicks off the corporate earnings reporting season when Alcoa posts their quarterly results. Market participants are anxiously waiting for these announcements to see how the economy is affecting earnings. Just as important as this past quarter's results are their forward-looking estimates. If revenue, earnings and projections from the big-named companies exceed expectations, stocks will likely rally. This would make bonds less appealing to investors and lead to bond selling. But if results are weaker than expected, indicating that the economy is stifling earnings, bonds will be more attractive to investors as stocks slide. That could help boost bond prices and help lower mortgage rates.

Overall, it is difficult to try to label one particular day as the most important this week. It is easy to say the least important will likely be tomorrow, but every other day has important data or other events that can cause significant movement in the markets and mortgage rates. The single most important report for the bond market is the CPI Friday morning, but Thursday’s data is not far behind. Wednesday’s Bernanke testimony could be huge also. The week's corporate earnings also have the potential to heavily influence bond trading and mortgage rates via stock market swings. Therefore, it is highly recommended to maintain fairly constant contact with your mortgage professional this week if still floating an interest rate.

Information courtesy of Joe Patterson with Princeton Capital (408)674-7438

This law would make it a felony if a parent or guardian fails to report a missing child immediately! It is such a small thing that we can do for Caylee...

Every year my husband wants to plan a Summer bash...not sure if timing is going to work this year but I always appreciate any helpful hints...hope these help you with your summer festivities!

How do you make your summertime party the event of the season? A few tips will go a long way in ensuring that your guests will remember the day long after the heat of the summer gives way to cool autumn days.

This holiday-shortened week brings us a couple of economic reports to drive the markets and mortgage rates, but one of them is highly important. It is a shortened week with the markets closed tomorrow. With a couple days that have little data or reports scheduled that are not considered important, it us quite likely that the stock markets will have the biggest influence on the bond market and mortgage pricing more than one day this week.

The Commerce Department will post May's Factory Orders data late Tuesday morning, which is similar to the Durable Goods Orders report that was released last week. The biggest difference is that this week's report covers both durable and non-durable goods. It usually doesn't have as much of an impact on the bond market as the durable goods data does, but can lead to changes in mortgage pricing if it varies greatly from forecasts because it measures manufacturing sector strength. Current expectations are showing a 1.0% increase in new orders from April's levels. A decline in orders would be considered good news for the bond market and could help lower mortgage rates slightly Tuesday.

Wednesday has a couple of reports that likely will not directly influence mortgage rates unless they show significant surprises, but since it is a light week they are worth mentioning. The first two are employment-related releases from private-sector entities. They will give us different opinions on the labor market, but unless they show surprising strength or weakness, they will probably have little impact on mortgage rates Wednesday morning.

The Institute for Supply Management (ISM) will post their Services Index for June late Wednesday morning. This index is somewhat similar to last Friday's ISM Manufacturing Index but tracks sentiment at the services level. It has the potential to impact bond trading and mortgage rates if it shows a sizable variance from forecasts, particularly when little other data is being posted. However, it usually has little influence on mortgage pricing and cannot be considered a key report. Current forecasts are calling for a reading of 54.0, which would be a decline from May's reading.

The last data of the week is arguably the single most important report we see each month. The Labor Department will post June's unemployment rate, number of new payrolls added or lost and average hourly earnings early Friday morning. These are considered to be very important readings of the employment sector and can have a huge impact on the financial markets. The ideal scenario for the bond market is rising unemployment, a large decline in payrolls and no change in earnings. Weaker than expected readings would likely help boost bond prices and lower mortgage rates Friday. However, stronger than expected readings could be extremely detrimental to mortgage pricing. Analysts are expecting to see the unemployment rate remain at 9.1%, with 80,000 jobs added and a 0.2% rise in earnings.

Overall, I am expecting to see a fairly quiet first day or so, but activity pick up drastically late in the week. The most important day is Friday, but the stock markets will also heavily affect trading if they rally or go into a sell-off.

A good porch, with shade, views, and cool breezes, is the perfect place to spend a summer afternoon, hence their common association with antebellum Southern plantations, Gone With The Wind and all that.

RISMEDIA, June 23, 2011—Existing-home sales were down in May as temporary factors and financing problems weighed on the market, according to the National Association of REALTORS®.

RISMEDIA, June 21, 2011—Greg Rand (@gsrand), CEO of OwnAmerica.com hosts “Rand on Real Estate” on 77WABC Radio in New York - this week’s discussion - it has never been a better time to become a landlord.

This will likely prove to be another active week in terms of mortgage rate movement due to the economic data and other events that are scheduled, but we may see less intra-day swings than we did the past two weeks. There are four economic reports scheduled for release in addition to another Federal Open Market Committee (FOMC) meeting.

There is no relevant economic news scheduled for release tomorrow. Tuesday brings us the first data with the release of May's Existing Home Sales report. The National Association of Realtors will give us figures on home resales late Tuesday morning. This data helps us measure housing sector strength and mortgage credit demand, but it usually takes a large variance from forecasts for it to cause a noticeable change to mortgage rates. It is expected to show a decline in home sales from April to May.

Wednesday’s only event is the adjournment of the FOMC meeting that began Tuesday. It is widely expected that Mr. Bernanke and company will not change key short-term interest rates at this meeting. But, as we have seen so many times in the past, it is the post meeting statement that often creates the most volatility in the markets. They could give an opinion of the overall economy or inflation, hinting at a possible future move or lack of one. Statements like these could cause a knee-jerk reaction in the markets and possibly mortgage pricing after the 12:30 PM ET adjournment.

Thursday's only report is the release of May's New Home Sales. It is similar to Tuesday's Existing Home Sales report, but tells us how well sales of newly constructed homes were last month. It is also expected to show a decline in sales, but will likely not have much of an impact on mortgage rates because this data tracks only the 15% of home sales that Tuesday's data does not.

There are two reports being released Friday morning. The first is the final reading to the 1st Quarter Gross Domestic Product (GDP). The GDP is the sum of all products and services produced in the U.S. and is considered to be the best measurement of economic growth or contraction. However, this data is quite aged now (covers January through March) and will likely have little impact on the bond market or mortgage pricing unless it varies greatly from previous readings. Market participants are looking more towards next month’s release of this quarter’s GDP reading. Last month's first revision showed a 1.8% rise in the GDP, which is what analysts are expecting to see again.

May's Durable Goods Orders will also be posted early Friday morning, giving us an indication of manufacturing sector strength. It is known to be quite volatile from month to month and is expected to show an increase of 1.0% in new orders from April to May. A large decline would be the ideal scenario for the bond market and would likely lead to a decline in mortgage pricing because it would indicate manufacturing sector weakness.

Overall, tomorrow will likely be the quietest day of the week unless the stock markets stage a rally or sizable sell-off. The most active should be Wednesday with the FOMC meeting adjourning or Friday due to the Durable Goods report being posted that day. Tuesday's news may also affect mortgage rates, but likely not as much as other days.

Information courtesy of Joe Patterson (408)674-7438 with Princeton Capital

Write a comment about this article.

Write a comment about this article.